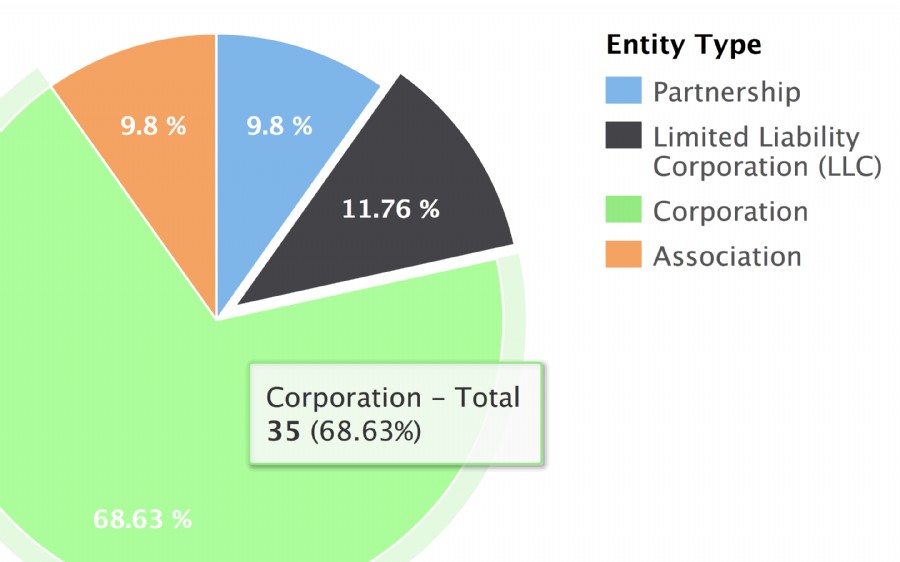

When starting a business venture, one of the first decisions to make is to determine what form of business entity to establish. The business structure you choose will have legal and tax implications, so it is very important to understand at least the basic differences amongst the most common forms of business entities; namely:

- Sole Proprietorships (or DBA);

- Partnerships;

- Corporations;

- Limited Liability Companies (LLC);

- Cooperatives;

SOLE PROPRIETORSHIPS (or DBA)

A sole proprietorship (also known as DBA, short for “doing business as”) is the simplest and least expensive structure that may be chosen to start a business.

It is an unincorporated entity owned and run by one individual with no distinction between the company and its owner, who is entitled to all profits and has unlimited personal liability for all the company’s debts, obligations and losses.

Because the sole proprietor and its business are one and the same, there is no legal separation between him/her and the business, with the consequence that the business itself is not taxed separately. The sole proprietorship’s income or loss becomes the individual’s income or loss, which means that it must be included in his/her personal tax return.

PARTNERSHIPS

A partnership is a vehicle where two or more people share ownership. Generally, each partner contributes to all aspects of the business, including money, property, labor and skills and will share in the profits and losses of the

CORPORATIONS

A corporation is an independent legal entity that is separate from the people – so called “shareholders” – who own and may control and manage it. This means that the corporation itself, not the shareholders who own it, is held legally liable for its actions and the debts incurred, while the shareholders have limited legal and financial liability. Generally, shareholders cannot be sued individually for corporate wrongdoings and their personal assets are protected from the creditors of the corporation (they can generally only be held accountable for the amount of capital committed to invest in the company).

Shareholders elect a Board of Directors which make business decisions and oversee policies, and appoint the Officers (President, Treasurer and Secretary), responsible for the day-to-day operations.

LIMITED LIABILITY COMPANIES (LLC)

The Limited Liability Company, also known as LLC, is a relatively new form of business created in 1977 in Wyoming and now recognized in all 50 states and the District of Columbia.

It can be best described as a hybrid between a corporation and a partnership because it provides the limited liability features of a corporation and the tax efficiencies and operational flexibility of a partnership.

Owners of an LCC are called members and may include individuals and entities (whether domestic or not).

The peculiarity of this kind of company is that, just like shareholders of a corporation, all LCC owners are protected from personal liability for business debts and claims: only LCC assets are used to pay off business debts, while owners stand to lose only the money that they have invested in the company. However, a LCC doesn’t have the corporate formalities (Board meetings, Shareholders meeting, minutes, etc.) or extra levels of management (Shareholders, Directors, Officers), but the easy management of a partnership. Moreover, unlike “C” corporations, LCCs are not taxed as a separate business entity. Instead, business income is “passed through” the business to the members, who report their share of profit – or losses – on their personal tax returns, just like the owners of a partnership would.